Taking your first loan can feel confusing and even a little scary. There are many terms like interest rate, EMI, and credit score that may seem complicated at first. That’s why having a clear beginner loan guide is so important before making any borrowing decision.

A loan can be a helpful financial tool when used wisely. Whether you need money for education, buying a car, starting a small business, or handling an emergency, the right loan can support your goals. However, borrowing without understanding how loans work can lead to financial stress.

In this guide, you’ll learn the basics of loans, how they work, different types of loans, and smart tips to borrow responsibly. By the end, you’ll feel more confident and prepared to make better financial decisions. beginner loan guide

What Is a Loan? (Basic Explanation)

A loan is an agreement between a borrower and a lender where the lender provides money that must be repaid within a fixed period along with interest. It is a common financial tool that helps individuals and businesses manage large expenses without paying the full amount upfront. beginner loan guide

Main Components of a Loan

To clearly understand a loan, it is important to know its basic parts. The principal is the original amount of money you borrow from the lender. The interest is the extra amount you pay as the cost of borrowing that money, usually calculated as a percentage of the principal. The loan tenure is the time period given to repay the loan, which can range from a few months to several years. The EMI (Equated Monthly Installment) is the fixed monthly payment that includes both principal and interest. beginner loan guide

Why Do People Take Loans?

People take loans for many important reasons. Some borrow money to buy a home or car, while others need funds for education, medical emergencies, weddings, or starting a small business. Loans make it possible to handle big expenses by spreading payments over time, making them more manageable. beginner loan guide

Is Taking a Loan a Good Idea?

Taking a loan can be a smart decision if you plan carefully and borrow responsibly. It allows you to achieve goals faster, but it also creates a financial obligation. Before applying for a loan, you should understand the interest rate, total repayment amount, and whether the monthly EMI fits your budget. Making informed decisions helps you avoid financial stress in the future. beginner loan guide

How Loans Work Step-by-Step

Understanding the loan process in detail helps beginners avoid confusion and make better financial decisions. Below is a more detailed explanation of how loans work from start to finish. beginner loan guide

Step 1: Identify Your Need

Before applying, you should clearly understand why you need the loan and how much money is required. Borrowing only what you truly need helps reduce interest costs and keeps your monthly payments manageable. beginner loan guide

Step 2: Check Your Eligibility

Each lender has eligibility criteria based on age, income, employment type, and credit score. Checking these requirements beforehand increases your chances of approval and saves time. beginner loan guide

Step 3: Compare Lenders and Loan Offers

Different banks and lenders offer different interest rates, processing fees, and repayment terms. Comparing multiple options helps you choose the most affordable and suitable loan for your situation. beginner loan guide

Step 4: Submit Your Application

Once you select a lender, you complete the loan application form and submit necessary documents such as ID proof, income proof, and bank statements. Some lenders allow fully online applications, making the process quick and convenient.

Step 5: Verification and Credit Assessment

The lender reviews your documents and checks your credit score to evaluate your repayment ability. A higher credit score often results in better interest rates and faster approval.

Step 6: Loan Approval and Offer Letter

If approved, the lender sends you a loan agreement or offer letter. This document includes important details like loan amount, interest rate, EMI amount, tenure, processing fees, and penalties. Reading this carefully is very important before signing.

Step 7: Loan Disbursement

After you accept the agreement, the loan amount is transferred to your bank account or directly to the seller in case of home or car loans. The disbursement may take a few hours to a few days, depending on the lender.

Step 8: EMI Repayment Begins

Repayment usually starts the following month. You must pay your EMI on time every month. Many lenders offer auto-debit options to avoid missing payments.

Step 9: Handling Prepayment or Foreclosure

Some borrowers choose to repay the loan early to save on interest. However, some lenders may charge prepayment or foreclosure fees, so it’s important to check these terms in advance.

Step 10: Loan Closure

Once all EMIs are paid, the loan is officially closed. You should collect a loan closure certificate from the lender. For secured loans, your collateral documents are returned after full repayment.

By understanding each step clearly, beginners can borrow confidently, avoid hidden surprises, and manage their finances responsibly.

you may also like to read these posts;

How Personal Loans Work: Beginner’s Complete Guide

How to Check Loan Eligibility and Get Approved Quickly

Safe Loan Tips for Easy Approval and Smart Borrowing

Loan Approval Tips to Boost Your Approval Chances

Loan Basics for Beginners: Tips for Smart Borrowing

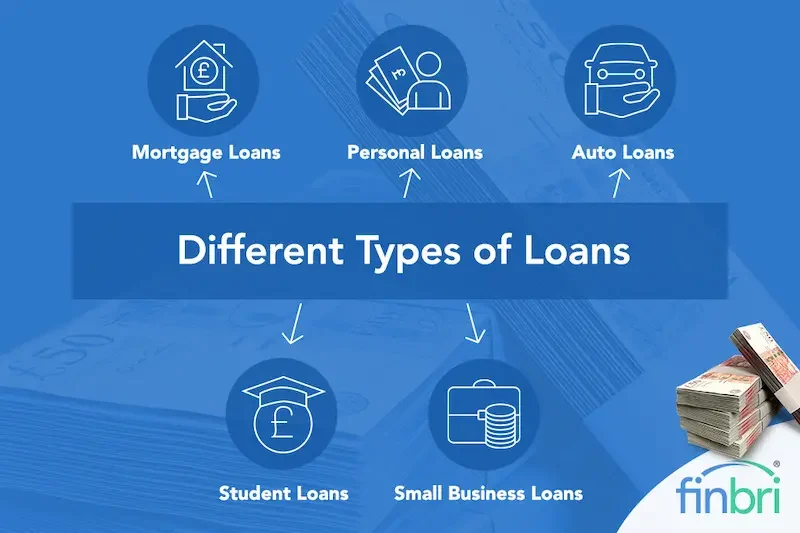

Types of Loans for Beginners

When starting out with borrowing, it’s important to know the different loan options available. Each type serves a different purpose, and choosing the right one can save you money and avoid unnecessary stress.

1. Personal Loan

A personal loan is an unsecured loan, which means you don’t need to provide collateral. It can be used for a variety of purposes, including medical emergencies, weddings, travel, or daily expenses. Personal loans are convenient but often come with higher interest rates compared to secured loans.

2. Home Loan

Home loans are designed to help you buy, build, or renovate a house. They usually have long repayment periods, sometimes up to 20–30 years. Because the house acts as collateral, interest rates are generally lower than personal loans. This makes home loans a popular choice for beginners looking to invest in property.

3. Car Loan

A car loan allows you to purchase a new or used vehicle. The car itself usually acts as security for the loan. Car loans typically have shorter repayment tenures than home loans, and monthly EMIs are designed to fit within a beginner’s budget. beginner loan guide

4. Student Loan

Student loans help cover tuition fees, books, and living expenses while you are studying. Many student loans offer flexible repayment options, with repayment starting only after graduation. Some also offer lower interest rates to support education. beginner loan guide

5. Business Loan

Business loans are intended for starting or expanding a business. Lenders often require a detailed business plan and proof of income. For beginners looking to start a small business, these loans provide the necessary funds without dipping into personal savings. beginner loan guide

6. Gold Loan

A gold loan allows you to borrow money by pledging gold jewelry as collateral. These loans are usually approved quickly and offer lower interest rates because they are secured. They are ideal for urgent financial needs and short-term borrowing.

7. Credit Card Loan

Some banks and financial institutions provide instant loans through credit cards. These are easy to access but come with higher interest rates if not repaid within the due date. They are suitable for small, short-term borrowing. beginner loan guide

8. Payday Loan

Payday loans are small, short-term loans meant to cover urgent expenses until your next paycheck. They are quick to obtain but usually come with very high interest rates, so they should be used cautiously. beginner loan guide

9. Agricultural or Farmer Loan

These loans are designed for farmers to buy seeds, fertilizers, or equipment. Interest rates may be lower due to government subsidies, making them beginner-friendly for those in agriculture. beginner loan guide

10. Microfinance Loan

Microfinance loans are small loans offered to individuals who may not have access to traditional banking. They are ideal for beginners with limited income who need a small amount to start a business or cover urgent needs. beginner loan guide

By understanding these loan types, beginners can make informed decisions and choose a loan that fits their purpose, repayment ability, and financial goals. Always compare interest rates, repayment terms, and processing fees before applying.

What is a loan?

A loan is money borrowed from a bank, lender, or financial institution that you must repay over time with interest. It allows you to afford expenses without paying the full amount upfront.

What is the difference between secured and unsecured loans?

Secured Loan: Requires collateral like property, gold, or a car. Usually has lower interest rates.

Unsecured Loan: Does not require collateral but may have higher interest rates.

What is a credit score and why does it matter?

A credit score is a number that represents your creditworthiness. A higher score increases your chances of loan approval and helps you get lower interest rates.

Conclusion

Taking a loan for the first time can seem overwhelming, but understanding the basics makes the process much easier. Loans are financial tools that can help you achieve important goals, such as buying a home, paying for education, starting a business, or handling emergencies. beginner loan guide

As a beginner, it is important to choose the right type of loan, understand the terms, compare interest rates, and plan your monthly payments carefully. Making timely EMI payments and borrowing only what you can repay will help you avoid financial stress and build a strong credit history.

By using loans responsibly, you can meet your financial needs, achieve your goals faster, and gain confidence in managing your personal finances. A well-planned loan can be a stepping stone to financial growth and stability.