Getting a loan can be exciting, but it can also be confusing for first-time borrowers. Lenders do not approve every loan application automatically—they check whether you meet certain eligibility criteria before giving you the funds. Knowing these criteria in advance can save time, avoid rejection, and help you plan your finances better.

Loan eligibility depends on factors such as age, income, employment status, credit score, existing debts, and the type of loan you are applying for. Whether you want a personal loan, home loan, car loan, or business loan, understanding these factors makes borrowing safer and easier.

This guide will explain all the important aspects of loan eligibility, how it is calculated, and tips to improve your chances of approval. By the end, you will know exactly what lenders look for and how to prepare for a successful loan application. loan eligibility guide

What Is Loan Eligibility?

Loan eligibility is the set of conditions or criteria that a lender uses to decide whether you qualify for a loan. In simple terms, it’s the measure of your ability to borrow money and repay it on time. loan eligibility guide

Lenders assess eligibility to ensure that the borrower can handle the repayment without defaulting. The main goal is to reduce the risk for both the borrower and the bank. loan eligibility guide

Key Factors That Determine Loan Eligibility:

- Income and Salary – Your monthly or annual income shows the lender how much you can afford to repay.

- Credit Score – A higher credit score (usually 700+) indicates good financial discipline, increasing approval chances.

- Age and Employment Status – Most lenders have minimum and maximum age limits and prefer stable employment.

- Existing Debts – If you already have multiple loans, it may affect your eligibility.

- Loan Type and Amount – Different loans (personal, home, car, business) have their own criteria. loan eligibility guide

Why Loan Eligibility Matters:

- Helps you know how much you can borrow.

- Saves time by avoiding applications you’re unlikely to get approved for.

- Allows you to compare lenders and choose the best terms.

By understanding loan eligibility, you can prepare better, improve your financial profile, and increase the chances of your loan being approved quickly. loan eligibility guide

Types of Loans and Their Eligibility Criteria

Different loans serve different purposes, and each type has its own eligibility requirements Understanding these requirements helps you prepare a stronger application and increases your chances of approval

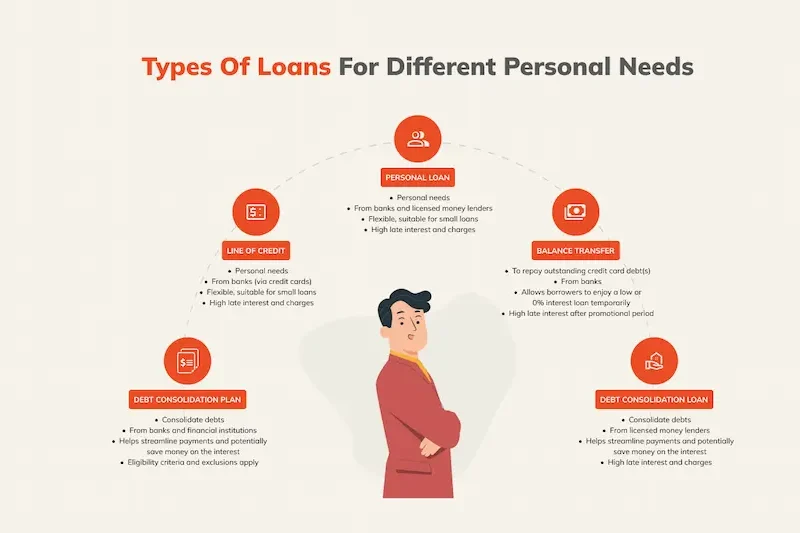

Personal Loans

Personal loans are usually unsecured and can be used for medical expenses, travel, weddings, or debt consolidation They are popular because of their flexibility and quick processing Eligibility typically includes a minimum age of 21 years, a stable source of income, and a good credit score Lenders may also consider existing debts The loan amount is often based on monthly income and repayment capacity Personal loans generally do not require collateral but may have higher interest rates compared to secured loans

Home Loans

Home loans are designed for purchasing property or construction Eligibility factors include age (usually between 21 and 65 years), steady income, and a good credit history Lenders also check property documents, legal approvals, and the applicant’s debt-to-income ratio Providing a higher down payment can increase eligibility and lower EMIs Home loans usually offer longer repayment periods, making them more affordable over time

Car Loans

Car loans help individuals buy new or used vehicles Eligibility requirements include being at least 21 years old, having a stable income, and maintaining a good credit score Lenders may offer better terms to salaried employees compared to self-employed individuals The loan-to-value ratio (loan amount compared to the car price) is important A lower ratio increases approval chances and may reduce interest rates

Business Loans

Business loans support startups, expansions, or working capital needs Lenders often require at least 1–2 years of business operations, financial statements, profitability records, and creditworthiness of the business owners A well-prepared business plan, clear revenue projections, and proper documentation improve approval chances Business loans can be secured (requiring collateral) or unsecured (higher interest rates) depending on the lender and loan type

Education Loans

Education loans are meant for students pursuing higher studies domestically or abroad Eligibility includes admission to a recognized course or institution, a co-applicant (usually a parent or guardian) with a stable income, and a good credit history of the co-applicant Many education loans offer lower interest rates and flexible repayment options Some lenders provide moratorium loan eligibility guideperiods until the student completes the course

Gold Loans

Gold loans allow borrowers to pledge gold jewelry as collateral These loans are usually fast and easy to process Eligibility mainly requires ownership of gold and proof of identity Lenders also consider the weight and purity of the gold The loan amount is calculated as a percentage of the gold’s market value Interest rates are generally lower compared to unsecured loans loan eligibility guide

Payday or Short-Term Loans

These are small, short-term loans for urgent financial needs Eligibility is simple and often only requires proof of income and identity The loan amounts are typically smaller, but interest rates can be higher due to short repayment periods These loans are useful for emergencies but should be used carefully to avoid debt traps loan eligibility guide

Key Factors Affecting Loan Eligibility

Knowing what affects loan eligibility can save time and help you plan better Lenders look at multiple factors to decide whether to approve your loan and under what terms Understanding these factors allows you to take proactive steps to improve your chances loan eligibility guide

Credit Score and Credit History

Your credit score is one of the most important factors in loan approval It reflects your financial discipline and repayment behavior A higher score (usually 700 or above) shows you are a responsible borrower, which increases your chances of approval and may lower interest rates Lenders also check your credit history, including past loans, credit card payments, and defaults Avoid missing payments, reduce overdue debts, and regularly check your credit report to keep it healthy loan eligibility guide

Income and Financial Stability

Lenders assess your monthly or annual income to ensure you can repay the loan comfortably Your total income, sources of income, and stability matter A regular salary, steady business revenue, or a combination of both improves eligibility Lenders also look at your debt-to-income ratio, which is the percentage of your income used to pay existing debts Keeping this ratio low strengthens your application loan eligibility guide

Employment Type and Job Stability

Stable employment or a long-standing business makes you a more reliable borrower Salaried individuals with a permanent job are usually preferred Freelancers or self-employed applicants may need to provide additional documents like tax returns, bank statements, and profit-and-loss reports to prove income consistency loan eligibility guide

Existing Debts and Liabilities

If you already have loans, credit card dues, or other financial obligations, lenders consider how these will affect your ability to repay the new loan Too many existing debts can lower eligibility or lead to rejection Paying off high-interest loans and maintaining a healthy credit balance improves your chances loan eligibility guide

Age and Legal Residency

Most lenders set a minimum and maximum age for borrowers Minimum age ensures you are legally allowed to borrow, while maximum age ensures the loan can be repaid within your working years Some loans like home or education loans may have stricter age limits Proof of identity, address, and residency is mandatory loan eligibility guide

Loan Type, Amount, and Tenure

Different loans have different eligibility standards Home loans, business loans, and personal loans vary in requirements Higher loan amounts or longer tenures usually require stronger income proof, better credit scores, and sometimes collateral Some loans like gold or vehicle loans may be easier to get because they are secured loan eligibility guide

Collateral and Security (If Applicable)

Secured loans like home, car, or gold loans require collateral Lenders assess the value and ownership of the asset Collateral reduces the lender’s risk, often improving your eligibility and offering lower interest rates loan eligibility guide

Additional Factors

Some lenders also consider your educational background, profession, or industry Stability in certain sectors may increase trust in repayment ability For business loans, a detailed business plan, revenue projections, and market credibility can significantly affect eligibility loan eligibility guide

Tips to Improve Loan Eligibility

- Maintain a good credit score by paying bills and EMIs on time

- Reduce existing debts to lower your debt-to-income ratio

- Keep a stable job or business record

- Save for a down payment if applying for secured loans

- Ensure all documents are accurate and complete before applying

By understanding these key factors, you can actively improve your financial profile and increase your chances of loan approval Preparing in advance not only speeds up the process but may also help you secure better interest rates and loan terms loan eligibility guide

you may also like to read these posts;

How Personal Loans Work: Beginner’s Complete Guide

Safe Loan Tips for Easy Approval and Smart Borrowing

Loan Approval Tips to Boost Your Approval Chances

Loan Basics for Beginners: Tips for Smart Borrowing

How to Check Your Loan Eligibility

Checking your loan eligibility before applying helps you save time, avoid rejections, and plan your finances better Lenders want to know upfront whether you can repay the loan, and being prepared gives you an advantage loan eligibility guide

Use Online Loan Eligibility Calculators

Almost every bank and financial institution provides an online loan eligibility calculator These tools are free and easy to use You simply enter: loan eligibility guide

- Your age

- Monthly or annual income

- Employment type (salaried, self-employed, or business)

- Existing loans or debts

- Desired loan amount and tenure

The calculator instantly shows your estimated loan eligibility and probable EMI This helps you understand what you can realistically borrow and which loan suits your financial situation loan eligibility guide

Check With Your Bank or Financial Institution

Visiting your bank or lender branch can give a more personalized assessment A bank representative will review your documents, income, and credit history They may provide a pre-approval certificate or estimate, which shows your borrowing power without a full application This is especially helpful for home and business loans

Fill Out Eligibility Forms

Many lenders offer simple forms online or offline where you submit basic details about your personal information, income, employment, and existing debts These forms allow lenders to quickly assess your eligibility and may also indicate if you need to improve your credit profile or income documentation before applying loan eligibility guide

Review Your Credit Report and Score

Your credit report is a key factor in loan eligibility Checking your report helps you:

- Confirm your credit score

- Identify any errors or discrepancies

- Ensure all past dues are cleared

A healthy credit report increases your chances of approval and may also lower interest rates If your report has mistakes, get them corrected before applying loan eligibility guide

Compare Multiple Lenders

Eligibility criteria vary across banks and NBFCs Comparing multiple lenders helps you:

- Identify which bank offers the highest loan amount for your profile

- Find the lowest interest rates and fees

- Understand different repayment options

Sometimes, even if one lender rejects your application, another may approve it due to more flexible criteria

Consider Pre-Approved Loans

Some banks provide pre-approved loans to existing customers based on their account history and transaction records Pre-approval gives you a clear idea of how much you can borrow and speeds up the loan process since the bank already has most of your financial information

Keep Your Documents Ready

While checking eligibility, it’s important to have these documents handy:

- Identity proof (ID card, passport, or driving license)

- Address proof (utility bills, rental agreement, or bank statement)

- Income proof (salary slips, bank statements, or business records)

- Credit history report

Having all documents ready makes the process faster and more accurate

Tips for Accurate Loan Eligibility Check

- Always provide accurate and up-to-date information

- Know your existing debts and liabilities

- Use online calculators for a quick estimate

- Compare different lenders before finalizing the loan

- Improve your credit score and reduce existing debts to increase eligibility

By taking these steps, you not only know how much loan you can get, but also understand the best lender, loan type, and repayment options for your financial situation Proper preparation makes the loan approval process faster, smoother, and more likely to succeed

What is loan eligibility?

Loan eligibility is the set of criteria that lenders use to decide if you qualify for a loan It depends on factors like income, credit score, employment, age, existing debts, and the type of loan

How can I check my loan eligibility?

You can check eligibility using online loan calculators, filling out forms at banks or lenders, reviewing your credit report, or visiting a bank branch for pre-approval

Does my credit score affect loan eligibility?

Yes, a higher credit score improves your chances of approval and can lower interest rates A low credit score may lead to rejection or higher interest rates

Conclusion

Understanding loan eligibility is the first step to making smart borrowing decisions By knowing what lenders look for—like income, credit score, employment, existing debts, and age—you can prepare your finances and increase your chances of approval Checking your eligibility beforehand saves time, avoids rejections, and helps you choose the best loan for your needs

Improving your eligibility is possible by maintaining a good credit score, reducing debts, keeping a stable job or business, and ensuring accurate documentation Different loans have different criteria, so comparing lenders and using online eligibility tools can help you find the right option for your situation

With careful planning and preparation, you can confidently apply for a loan, secure better interest rates, and achieve your financial goals Whether it’s a personal loan, home loan, car loan, business loan, or education loan, knowing your eligibility puts you in control and makes the borrowing process faster and smoother